Uncollectible accounts can significantly impact a company's financial health, particularly when it comes to accurate accounting practices. In the realm of finance and accounting, understanding how to handle uncollectible accounts is crucial for maintaining a clear financial picture. This article will explore the concept of uncollectible accounts, particularly focusing on the year-end adjusting entry of $4,500 made by companies. We will delve into the implications of uncollectible accounts, how they are recorded, and the importance of accounting adjustments in presenting a true and fair view of financial statements.

As businesses navigate the complexities of credit sales, they must also contend with the reality that not all debts will be collected. Uncollectible accounts, often referred to as bad debts, necessitate careful accounting to ensure that a company's financial statements accurately reflect its financial position. The year-end adjusting entry of $4,500 is a common occurrence, and understanding its implications will help business owners and accountants alike maintain compliance and transparency.

This article will provide you with an in-depth understanding of uncollectible accounts, the significance of the adjusting entry, and the broader impact on financial reporting. By the end of this discussion, you will have a comprehensive grasp of how to manage uncollectible accounts effectively.

Table of Contents

What Are Uncollectible Accounts?

Uncollectible accounts, often known as bad debts, refer to accounts receivable that a company has deemed unlikely to be collected. These accounts typically arise from credit sales where customers fail to pay their debts due to various reasons, such as financial difficulties or disputes.

Characteristics of Uncollectible Accounts

- Accounts that have been overdue for an extended period.

- Insolvency of the debtor.

- Bankruptcy filings by the customer.

- Disputes regarding the goods or services provided.

Importance of Uncollectible Accounts in Financial Reporting

Recognizing uncollectible accounts is essential for several reasons:

- Accuracy in Financial Statements: Failing to account for bad debts can overstate a company's assets and revenue.

- Cash Flow Management: Understanding uncollectible accounts helps businesses predict cash flows and manage finances effectively.

- Investor Confidence: Transparent reporting of uncollectible accounts fosters trust among investors and stakeholders.

Year-End Adjusting Entries Explained

Year-end adjusting entries are necessary to align the accounting records with the actual financial position of the company. These entries ensure that revenues and expenses are recognized in the correct accounting period, adhering to the accrual basis of accounting.

Types of Year-End Adjustments

- Accruals: Recognizing revenues and expenses that have been incurred but not yet recorded.

- Deferrals: Adjusting entries for cash received or paid in advance of the actual revenue or expense recognition.

- Estimates: Making reasonable estimates for uncollectible accounts, depreciation, and other financial aspects.

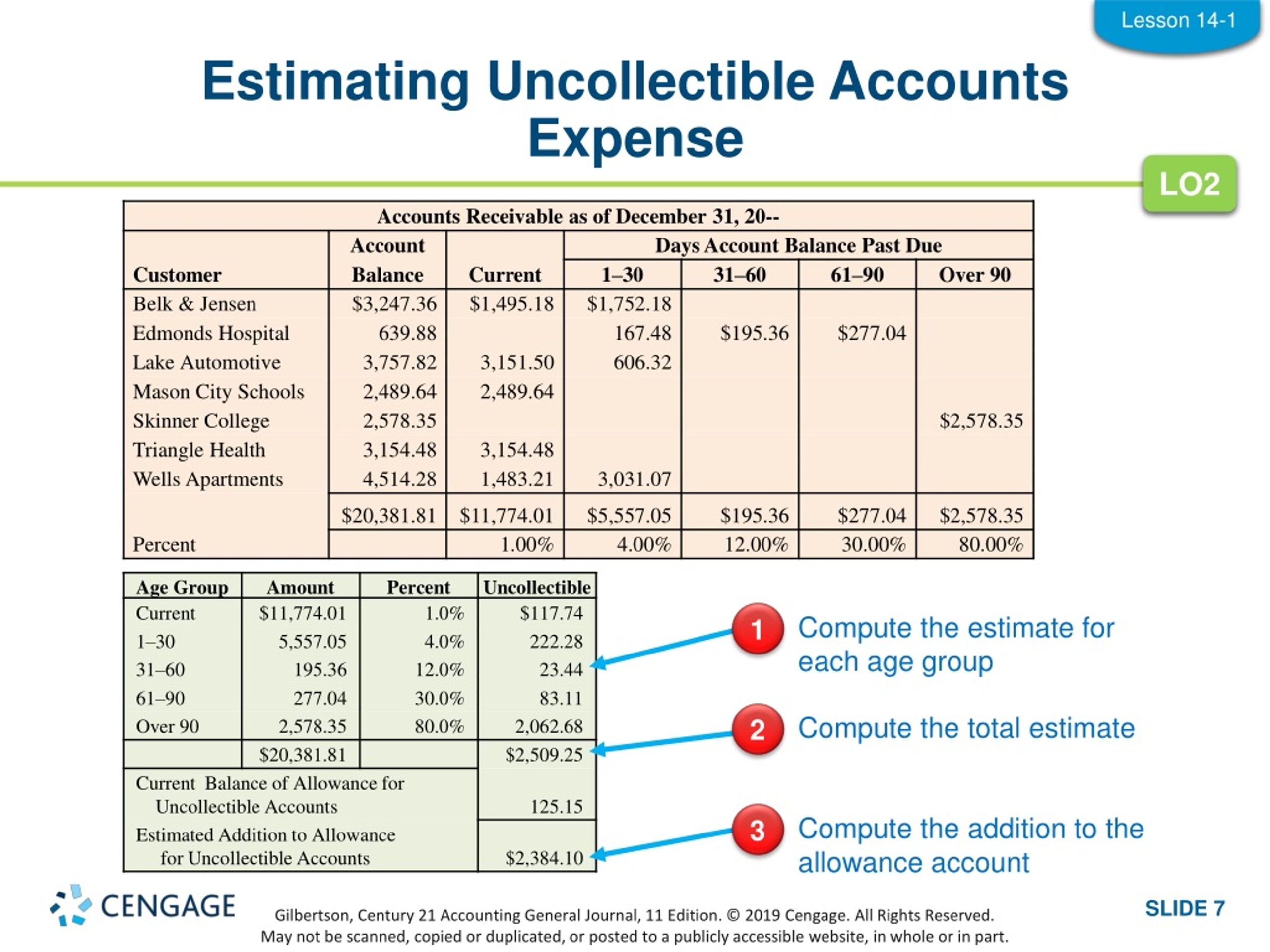

The $4,500 Adjusting Entry: A Case Study

In the context of uncollectible accounts, the $4,500 adjusting entry represents the estimated amount of accounts receivable that the company expects will not be collected by year-end. This entry is crucial for accurately reflecting the company's financial position.

Accounting for the Adjusting Entry

The adjusting entry for uncollectible accounts typically involves debiting the Bad Debt Expense account and crediting the Allowance for Doubtful Accounts. This approach ensures that the expenses are recognized in the same period as the related revenue.

Example Entry:

Bad Debt Expense $4,500 Allowance for Doubtful Accounts $4,500

Impact on Financial Statements

The year-end adjusting entry of $4,500 has several implications for a company's financial statements:

- Income Statement: The entry increases the Bad Debt Expense, thereby reducing the net income for the period.

- Balance Sheet: The Allowance for Doubtful Accounts reduces the total accounts receivable, providing a more accurate picture of the company's assets.

Accounting Standards and Regulations

Companies must adhere to accounting standards such as GAAP (Generally Accepted Accounting Principles) or IFRS (International Financial Reporting Standards) when accounting for uncollectible accounts. These standards dictate how to recognize, measure, and disclose bad debts.

Regulatory Compliance

Compliance with accounting standards is critical not only for accurate financial reporting but also for regulatory requirements imposed by governing bodies. Failure to comply can lead to severe penalties and loss of credibility.

Strategies for Managing Uncollectible Accounts

Organizations can implement several strategies to minimize the impact of uncollectible accounts:

- Credit Policies: Establishing clear credit policies to evaluate customer creditworthiness before extending credit.

- Regular Review: Conducting regular reviews of accounts receivable to identify potential bad debts early.

- Collection Efforts: Implementing proactive collection efforts, including follow-ups and payment reminders.

Conclusion

In conclusion, understanding uncollectible accounts and their implications for financial reporting is vital for any business. The year-end adjusting entry of $4,500 serves as a crucial step in ensuring the accuracy and reliability of financial statements. By recognizing and managing uncollectible accounts effectively, companies can maintain transparency, build investor confidence, and ultimately foster financial stability.

We encourage you to leave your thoughts in the comments below, share this article with others, or explore more insightful articles on our site!

Thank you for reading, and we look forward to welcoming you back for more expert insights into financial management!

ncG1vNJzZmivp6x7rLHLpbCmp5%2Bnsm%2BvzqZmm6efqMFuxc6uqWarlaR8trrCqKOlnZOptqO4xGaYnJufqru1v4ytpmaalWKBdnyPZquhnV2YvK68wKewrGWpmq6zecSnm2aZlJ%2FCtMDIp55mnZ6pv7p6x62kpQ%3D%3D