Understanding the difference between direct costs and indirect costs is crucial for businesses and individuals managing budgets and financial planning. In the realm of accounting and finance, these classifications play a significant role in determining the overall profitability and efficiency of an organization. This article aims to provide comprehensive insights into direct and indirect costs, offering definitions, examples, and their implications on financial statements.

As we delve deeper into the topic, we will explore various scenarios that illustrate the classification of costs, helping to clarify any confusion between these two categories. By the end of this article, readers will have a clearer understanding of how to classify each cost type, ensuring better financial decision-making.

This article is structured to be informative and engaging, with subheadings that break down the complexity of cost classifications. Whether you are a business owner, accountant, or simply someone interested in financial management, this guide will provide valuable knowledge on the topic.

Table of Contents

Definition of Direct and Indirect Costs

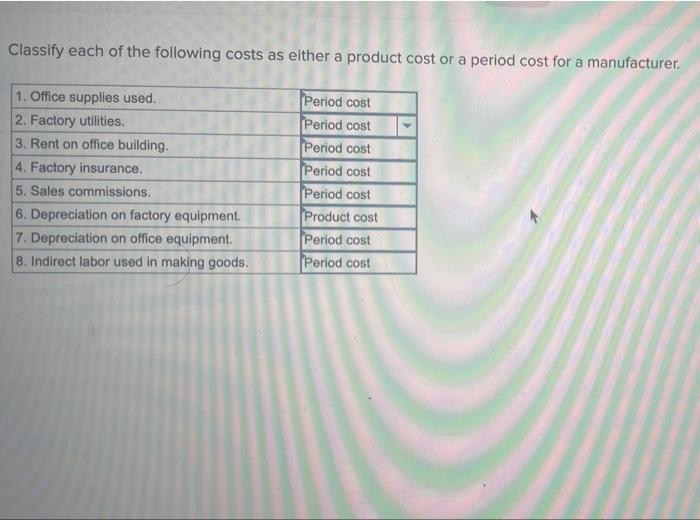

Direct costs are expenses that can be directly attributed to a specific product, service, or project. These costs are typically variable and fluctuate with production levels. Common examples include raw materials, labor costs, and manufacturing supplies.

On the other hand, indirect costs are expenses that are not directly tied to a specific product or service. These costs are often fixed and are incurred regardless of the level of production. Examples include utilities, rent, administrative salaries, and office supplies.

Key Differences

- Attribution: Direct costs can be traced directly to a cost object, while indirect costs cannot.

- Variability: Direct costs tend to vary with production levels, whereas indirect costs remain relatively stable.

- Examples: Direct costs include materials and labor, while indirect costs encompass overhead expenses.

Examples of Direct Costs

Identifying direct costs is essential for accurate budgeting and financial forecasting. Here are some common examples:

- Raw Materials: The cost of materials used in manufacturing a product.

- Direct Labor: Wages paid to employees who are directly involved in the production process.

- Manufacturing Supplies: Items consumed in the production of goods that can be directly linked to a product.

- Sales Commissions: Payments made to sales personnel directly related to the sale of products.

Examples of Indirect Costs

Indirect costs, although not directly tied to a specific product, are still essential for the overall functioning of a business. Here are some examples:

- Rent: The cost of leasing office or production space.

- Utilities: Expenses for electricity, water, and heating that support the entire operation.

- Administrative Salaries: Wages for employees who support the business but do not directly contribute to production.

- Depreciation: The gradual reduction in value of assets used in the business.

Importance of Classifying Costs

Classifying costs into direct and indirect categories is crucial for several reasons:

- Budgeting: Accurate classification helps in creating realistic budgets and forecasts.

- Pricing Strategies: Understanding direct costs allows businesses to set appropriate prices for their products.

- Profitability Analysis: By distinguishing between direct and indirect costs, businesses can assess their profitability more accurately.

- Cost Control: Effective classification enables better cost management and control measures.

Impact on Financial Statements

The classification of costs directly affects financial statements, particularly the income statement and balance sheet. Here's how:

- Income Statement: Direct costs are subtracted from revenue to calculate gross profit, while indirect costs are deducted to determine operating profit.

- Balance Sheet: Indirect costs often appear as assets (like prepaid expenses or accumulated depreciation) impacting the overall financial position.

Cost Allocation Methods

Cost allocation is the process of identifying, aggregating, and assigning costs to cost objects. Here are some common methods:

- Direct Allocation: Assigning direct costs to the specific cost object.

- Step-Down Method: Allocating indirect costs in a sequential manner to various departments or products.

- Activity-Based Costing (ABC): Allocating costs based on the activities that drive costs, providing a more accurate cost representation.

Business Implications of Cost Classifications

Understanding the difference between direct and indirect costs can have significant implications for business strategies:

- Investment Decisions: Knowing which costs are direct can influence decisions regarding product lines and services.

- Performance Evaluation: Classifying costs appropriately helps in evaluating departmental performance and efficiency.

- Tax Implications: Certain costs may be deductible for tax purposes; understanding classifications can optimize tax liabilities.

Conclusion

In conclusion, classifying costs as direct or indirect is essential for effective financial management. By understanding the definitions, examples, and implications of these cost types, businesses can make informed decisions that enhance profitability and operational efficiency. We encourage readers to assess their own financial practices and consider how effective cost classification can improve their outcomes.

For more insights on financial management and cost analysis, feel free to leave a comment or share this article with your network. Your engagement helps us provide even more valuable content in the future!

Thank you for reading! We hope to see you back on our site for more informative articles.

ncG1vNJzZmivp6x7rLHLpbCmp5%2Bnsm%2BvzqZmm6efqMFuxc6uqWarlaR8pLjArKqinqlisqKvx2amn2WknbJuss6lo6ivmaO0bq%2FOrKusZZGoeqJ5w6KpnpukYrCwv9NmpqtlkaN6qrrDoqmem6RisLC%2F02efraWc